I’ll be especially interested in seeing if this hire improves Workday’s positioning of its financial suite, where many of the sourcing, planning, and analytics pieces are there but Workday is still struggling to gain CFO mindshare and displace incumbents at the enterprise level.

And honestly, a lot of this is because Workday still approaches its business from an HR-first mindset that is clear when you look at their AI assistant announcements and partner announcements. it is not enough to just say “HR and finance” instead of HR in press releases when the actual products are still focused on talent management and individuals.

I would love to see Workday focus more on the office of the CFO and the idea of talent-and-skills based finance or finance for the innovation-based business, which requires talent and subject matter expertise. These are areas where traditional monolithic ERPs struggle and where smaller finance startups lack visibility to employee skills. Perhaps an analyst firm or consulting firm that Workday listens to will bring this up somewhere down the road.

Or perhaps Rob Enslin will get to flex the skills and positioning that he showed at SAP to push Workday forward into being a true enterprise software player rather than the HR specialist it is best known for being. The products are there, the roadmap and integrations are mostly in place, and the partnership intentions are there. Now for the go-to-market to solidify and for Workday Finance to be more than a me-too add-on.

The two aspects that I am most interested in across-the-board are:

The AI generated testing in Agentforce Testing Center where I think it is going to be vital for agents to be stress tested with the help of AI. It will obviously be easier for AI to bring up a wide variety of potential tests for an agent.

In the next few months, it will honestly be fairly trivial to build a standard agent within most large enterprise application platforms. But the challenge will be in testing these agents to run at enterprise scale, and with the variety of languages, context, grammar, jargon, and patois that may exist across the world in describing demands.

As George Bernard Shaw said “England and America are two countries separated by a common language”. and that can be multiplied by the countries and rules and backgrounds that global companies are trying to support with their Salesforce agents.

The other part that I most excited about is what Salesforce calls Utterance Analysis. This is a real time analysis on the usage of an agent based on the user inputs, requests, and query outputs. There has long been a struggle in translating event logs into useful data simply because logs are overwhelming. Salesforce’s efforts in this area are an important step forward in incorporating log data into more practical and consumable analytic form factors.

The one big question this press release does not tackle is around the orchestration and ongoing management of agent portfolios. Is it possible to find duplicate or similar agents and avoid the technical debt associated with managing 100s or thousands of agents going forward? It is a stated goal of Mark Benioff to have 1 billion agents built in a year. That is a great goal, but anyone who has ever worked IT or in sales ops knows that 1 billion custom objects, workflows, tests, agents, or any other documented item is always going to be an administrative burden.

Although I believe that Salesforce is making progress in this area, it is no secret that we look to Salesforce as providing a standard around enterprise governance for CRM and related applications. And I think this is an opportunity for Salesforce to show leadership in the ongoing management of agent portfolios at a time when the data and metadata in Salesforce are increasingly important to the valuation of the company as a strategic partner and to a publicly traded market capitalization.

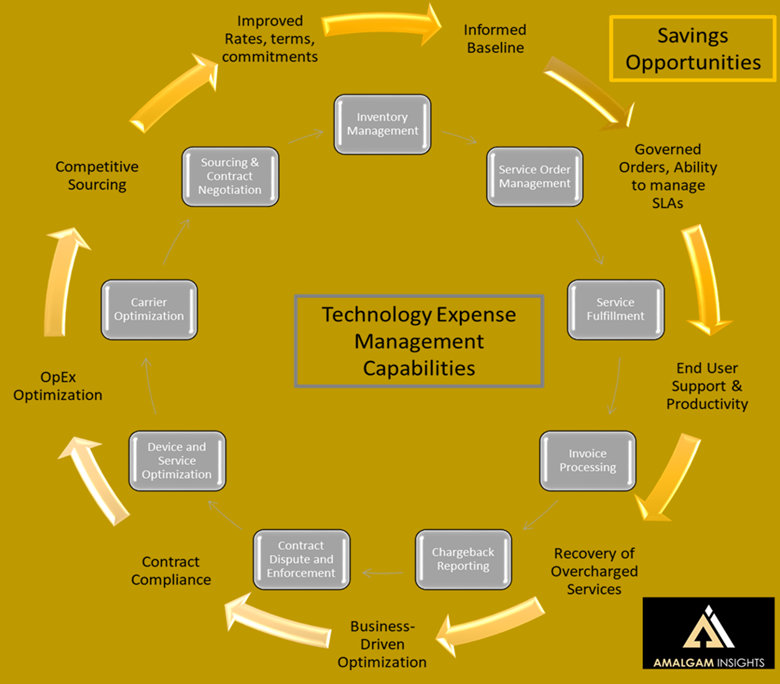

At Amalgam Insights, we’ve long championed the Technology Lifecycle Management approach to describe the many areas existing across IT FinOps to reduce costs across hyperscalers, data clouds, Software-as-a-Service, networking, enterprise mobility, and telecom costs. Usage optimization is not enough. Product rationalization is not enough. Contract negotiations are not enough. And when these opportunities are not bridged, additional opportunities fall by the wayside across the IT environment.

Technology Lifecycle Management

One of the most interesting trends of 2024 has been the FinOps Foundation’s initial steps into software management. As cloud FinOps starts entering the already-established worlds of SaaS management and network management, it will be interesting to see both where cloud FinOps’ comfort zone of massive usage and product tradeoffs help the more static worlds of software and telecom as well as where FinOps’ traditional struggles with business taxonomy, detailed sub-user chargebacks, and lack of contract detail start to push against the issues that you, I, and the rest of the IT world have been dealing with for the past 15+ years. Unlike Cloud FinOps, Software FinOps and Telecom FinOps have a long history of multi-user monitoring, usage, and cost management and to avoid cooperating with end-user requests for any type of market-wide billing or usage standardization.

For the past several months, I’ve been working on my SmartList of IT FinOps vendors (thank you to all the vendors and customers for your participation!) with a eye towards looking at vendors focused on bridging gaps between cloud FinOps and the rest of the IT world. Out of the 300+ vendors I look at from an IT expense lifecycle perspective, I’ve narrowed the list down to 15 vendors that I think are really doing something different, which will be our Distinguished Vendors. But I am also starting to find some interesting trends that make these distinguished vendors different from the extremely crowded portfolio of options that IT departments face.

Before getting to those, let’s just define what is not considered differentiated in 2024. Simply ingesting bills is not good enough. Being customer-centric and having attention to detail are considered table stakes if you cannot provide customers that vouch for your approach being quantitatively better than other competitors. Everybody I cover can support tagging. Cross-charging is a standard enterprise ask in RfX activity. Basic dashboards and analytics are standard (and if you haven’t chosen a high-performance analytics solution like Sisense or Sigma or Qrvey, you’re probably behind for supporting real-time changes). And everyone is competing against 2020s-era design standards for SaaS as a standard, especially with the flood of money that has gone into the data and code-centric Third Wave of FinOps.

First, as expected, top vendors are often finding now that they are the second or third solution chosen at the enterprise level. IT buyers have often focused on the “up and to the right” vendor landscape too much in their purchase of FinOps and IT expense management solutions with the assumption that these are commoditized solutions rather than the financial window to the pulse of the digital business. Although every business today likes to talk about how they have “digitally transformed” and are “data-driven,” the truth is that companies have not fully embraced data and digital business until the actual cost of data infrastructure, delivery, and data-related customer activities can be finally categorized and calculated. And without FinOps and IT expense solutions, the comparative data simply isn’t there at the bill of material (BOM) or component level that we take for granted in manufacturing or service level. A digital business lacking formal IT FinOps is like managing a hospital without knowing how many procedures are being done or a discrete manufacturing company not knowing how many parts it uses.

Second, there is a massive effort to utilize and translate tagging efforts into standard business categories. The FinOps insistence on tagging service elements across infrastructure and platform without alignment to larger corporate or IT frameworks is starting to collapse into its own form of technical debt. The combination of poor data quality, inconsistent or idiosyncratic tagging, poor mapping to existing categories, and lack of integration with existing birthright and foundational enterprise applications has led to the need for better metadata definition and mapping. Of course, the goal here is not simply to create a pristine metadata environment (although I do love well defined taxonomies and ontologies!), but to deeply align IT to business so that product, service, and revenue managers know which technologies are vital to their work.

Third, data integrations and a unified data layer are increasingly important across vendors. One of the most salient and welcome aspects of the latest wave of FinOps solutions is the data layer that provides visibility across hyperscalers, data clouds such as Databricks, Snowflake, and Cloudera, as well as observability solutions such as Datadog. From a tactical perspective, this data ingestion helps cloud architects and digital business leaders to track costs. But it also helps set up the FinOps practitioner as a central player in managing the business aspects of digital behavior. The cost of accessing, processing, and utilizing data will only increase with the emergence of AI as a new massive spend area within IT. And although this cost is under the direct supervision of the CTO and CFO right now in many cases, it will all eventually filter down to some level of IT FinOps as the complexity of these ecosystems becomes too immense. Many of today’s top solutions are proactively setting themselves to be this data layer for supporting the future of IT activity.

Fourth, the tradeoffs between defined hyperscalers, defined on-premises services, virtualized services, and containerized services continue to be a challenge and the current answer is often to split each of these categories into a separate management solution. This is not a sustainable approach and Amalgam Insights both expects and encourages market consolidation so that FinOps professionals can see more of their infrastructure and platform investments under the same umbrella.

Fifth, everybody likes to talk about “cloud economics” while ignoring the “economics” part of the puzzle. There is a lot of focus on the mathematical aspects of large scale optimization of usage. And I get it. Techies love working with big problems and algorithmic fixes and finding clever ways to discover null values and aggregating pennies into dollars. This skill set is often what makes technology contributors invaluable both in developing architecture and in root-cause analysis for large enterprise challenges. But it is only a piece of the puzzle when it comes to aligning the financial health of the enterprise with digital and cloud activity. At some point, this optimization needs to be tied to the less exciting tasks of invoice processing, cross-checking billing rates with existing rates and discounts, direct product tradeoffs both within and across hyperscaler providers, comparing contract terms, enforcing contracted KPIs and timeframes, and aligning cloud activity to new accounting rules and tax credits. All of this is part of the microeconomics of cloud. Simply looking at usage optimization makes you a unit-specific beancounter. A true cloud economist needs to understand how the cost of cloud shapes the rest of the business and how it needs to be structured, reinforced, and defined based on all business forces.

Sixth, the cost of IT FinOps is changing rapidly. The first generation of cloud FinOps solutions charged similarly to software management and telecom management vendors where enterprise spend was based on a percentage of spend. But the problem is that these approaches started to outgrow their value for clients that grew their cloud spend to $50 million or $100 million and literally realized they could build their own solution and support it in perpetuity. We have seen solutions like Capital One Slingshot or Netflix’s development of NetflixOSS Ice, now supported by Teevity based on corporate efforts that became commercial products. So, there is a lot of pressure to drive down the cost of IT FinOps back to a flat license rate or user-based pricing once spend gets to an enterprise-tier. This pressure is exacerbated by the vendor sprawl across FinOps. For vendors that are product-based, this will continue to be a trend while companies shifting to a managed services approach will be able to maintain pricing based on the overall maintenance of the FinOps environment across billing, accounting, optimization, procurement, vendor relationships, governance, and IT-business alignment.

Those are some of the big trends I’ve been seeing so far over the last several months. There is a lot of nuance here, which I’m looking forward to digging into as I finalize the FinOps SmartList and get to highlight the Distinguished Vendors: the top 5% of companies that stand out both in their results and their differentiation. Is there anything you think I missed? Or do you want to talk more about either your FinOps product or your current FinOps RfP work? If so, get in touch with me at briefings@amalgaminsights.com.

Sports has increasingly become a showcase for back-end business capabilities that have long eschewed the spotlight: analytics, data, accounting, etc…

This recent ESPN article on the Knicks showcases the importance of their contract pro and combining strategic procurement (contract negotiations, KPIs, expiration dates, payment terms, vendor and client responsibilities) with the accounting knowledge to enforce and fully leverage those terms. And the Knicks’ player procurement Brock Aller gets a nice glow-up here because of his expertise across these areas in his complex spend category: player contracts and options.

Basketball has increasingly made “cap-ology” or the management of each team’s salary cap an important topic, as it often defines the practical limits of how much a professional basketball team can choose to improve. There is a practical lesson here for strategic IT procurement (or really all procurement) professionals on how to structure, reallocate, and maximize IT investment on a fixed budget or within a budget cap. I especially like the use of laddered rates, date-specific cutoffs and performance, and the use of commoditized or overlooked assets to trade for cash or optionality are all mentioned or hinted at here.

Even if I’m not a fan, the resurgence of the New York Knicks is a great case for how procurement and accounting need to work more closely together, ideally with a bridge person, to maximize value.

Amalgam Insights recently had the privilege of attending Informatica World 2024. This is a must-track event for every data professional if for no other reason than Informatica’s market leadership across data integration, master data management, data catalog, data quality, API management, and data marketplace offerings. It is hard to have a realistic understanding of the current state of enterprise data without looking at where Informatica is. And at a time when data is front-and-center as the key enabler for high-quality AI tools, 2024 is a year where companies must be well-versed in the various levels of data governance, management, and augmentation needed to make enterprise data valuable.

Of course, Informatica has embraced AI fully, almost to the point where I wonder if there will be a rebrand to AInformatica later this year! But all kidding aside, my focus in listening to the opening keynote was in hearing about how CEO Amit Walia and a group of select product leaders, customers, and partners would help build the case for how Informatica increases business value from the CFO office’s perspective.

Of course, there are a variety of ways to create value from a Data FinOps (the financial operations for data management) perspective, such as eliminating duplicate data sources, reducing the size of data through quality and cleansing efforts, optimizing data transformation and analytic queries, enhancing the business context and data outputs associated with data, and increasing the accessibility, integration, and connectedness of long-tail data to core data and metadata. But in the Era of AI, there is one major theme and Informatica defined exactly what it is.

Everybody’s ready for AI except your data.

Informatica kicked off its keynote with an appeal to imagination and showing “AI come to life” with the addition of relevant, high-quality data. Some of CEO Amit Walia’s first words were in warning that AI does not create value and is vulnerable to negative bias, lack of trust, and business risks without access to relevant and well-contextualized data. His assertion that data management (of course, an Informatica strength) “breathes life into AI” is both poetic and true from a practical perspective. The biggest weakness in enterprise AI today is the lack of context and anchoring because of dirty data and missing metadata that were ignored in an era of Big Data when we threw everything into a lake and hoped for the best. Informatica faces the challenge of cleaning up the mess created over the past decade as both the number of apps and volume of data have increased by an order of magnitude.

From a customer perspective, Informatica provided context from two Chief Data Officers during this keynote: Royal Caribbean’s Rafeh Masood and Takeda’s Barbara Latulippe. Both spoke about the need to be “AI Ready” with a focus on starting with a comprehensive data management and integration strategy. Masood’s 4Cs strategy for Gen AI of Clarity, Connecting the Dots, Change Management, and Continual Learning spoke to the fundamental challenges of anchoring AI with data and creating a data-driven culture to get to AI. As Amit Walia stated at the beginning: everybody is ready for AI except your data.

Latulippe’s approach at Takeda provided some additional tactics that should resonate with financial buyers, such as moving to the cloud to reduce data center sites, purchasing data from a variety of sources to augment and improve the value of corporate data as an asset, and consolidating data vendors from eight to two and increasing the operational role of Informatica within the organization in the process. Latulippe also mentioned a 40% cost reduction from building a unified integration hub and a data factory investment that provided a million dollars in savings from improved data preparation and cleansing. (In using these metrics as a guidepost for potential savings, Amalgam Insights cautions that the financial benefits associated with the data factory are dependent on the value of the work that data engineers and data analysts are able to pursue by avoiding scut work: some companies may not have additional data work to conduct while others may see even greater value by shifting labor to AI and high business value use cases.)

Amit Walia also brought four of Informatica’s product leaders on stage to provide roadmaps across Master Data Management, Data Governance, Data Integration, and Data management. Manouj Tahilani, Brett Roscoe, Sumeet Agrawal, and Gaurav Pathak walked the audience through a wide range of capabilities, many of which were focused on AI-enhanced methods of tracking data lineage, creating pipelines and classifications, and improved metadata and relationship creation above and beyond what is already available with CLAIRE, Informatica’s AI-powered data management engine.

Finally, the keynote ended with what has become a tradition: enshrining the Microsoft-Informatica relationship with a discussion from a high-level Microsoft executive. This year, Scott Guthrie provided the honors in discussing the synergies between Microsoft Fabric and Informatica’s Data Management Cloud.

Recommendations for the CFO Looking at Data Challenges and CIOs seeking to be financial stewards

Beyond the hype of AI is a new set of data governance and management responsibilities that must be pursued if companies are to avoid unexpected AI bills and functional hallucinations. Data environments must be designed so that all business data can now be used to help center and contextualize AI capabilities. On the FinOps and financial management side of data, a couple of capabilities that especially caught my attention were:

IPU consumption and chargeback: The Informatica Data Management Cloud, the cloud-based offering for Informatica’s data management capabilities, is priced in Informatica Pricing Units based on its billing schedule. The ability to now chargeback capabilities to departments, locations, and relevant business units is increasingly important in ensuring that data is fully accounted for as an operational cost or as a cost of goods sold, as appropriate. The Total Cost of Ownership for new AI projects cannot be fully understood without understanding the data management costs involved.

Multiple mentions of FinOps, mostly aligned to Informatica’s ability to optimize data processing and compute configurations. CLAIRE GPT is expected to further help with this analysis as it provides greater visibility to the data lineage, model usage, data synchronization, and other potential contributors to high-cost transactions, queries, agents, and applications.

And the greatest potential contribution to data productivity is the potential for CLAIRE GPT to accelerate the creation of new data workflows with documented and governed lineage from weeks to minutes. This “weeks to minutes” value proposition is fundamentally what CFOs should be looking for from a productivity perspective rather than more granular process mapping improvements that may promise to shave a minute off of a random process. Grab the low-hanging fruit that will result in getting 10x or 100x more work done in areas where Generative AI excels: complex processes and workflows defined by complex human language.

CFO’s should be aware that, in general, we are starting to reach a point where every standard IT task that has traditionally taken several weeks to approve, initiate, assign resources, write, test, govern, move to production, and deploy in an IT-approved manner is becoming either a templated or a Generative AI supported capability that can be done in a few minutes. This may be an opportunity to reallocate data analysts and engineers to higher-level opportunities, just as the self-service analytics capabilities a decade ago allowed many companies to advance their data abilities from report and dashboard building to higher-level data analysis. We are about to see another quantum leap in some data engineering areas. This is a good time to evaluate where large bottlenecks exist in making the company more data-driven and to invest in Generative AI capabilities that can quickly help move one or more full-time equivalents to higher value roles such as product and revenue support or optimizing data environments.

Based on my time at Informatica World, it was clear that Informatica is ready to massively accelerate standard data quality and governance challenges that have been bottlenecks. Whether companies are simply looking for a tactical way to accelerate access to the thousands of apps and data sources that are relevant to their business or if they are more aggressively pursuing AI initiatives in the near term, the automation and generative AI-powered capabilities introduced by Informatica provide an opportunity for companies to step forward and improve the quality and relevance of their data in a relatively cost-effective manner compared to legacy and traditional data management tools.

This Week in Enterprise Tech, brought to you by the DX Report’s Charles Araujo and Amalgam Insights’ Hyoun Park, explores six big topics for CIOs across innovation, the value of data, strategic budget management, succession planning, and enterprise AI.

1) We start with the City of Birmingham, which is struggling with its SAP to Oracle migration. We discuss how this IT project has shifted from the promise of digital transformation to the reality of being in survival mode and the cautions of mistaking core services for innovation.

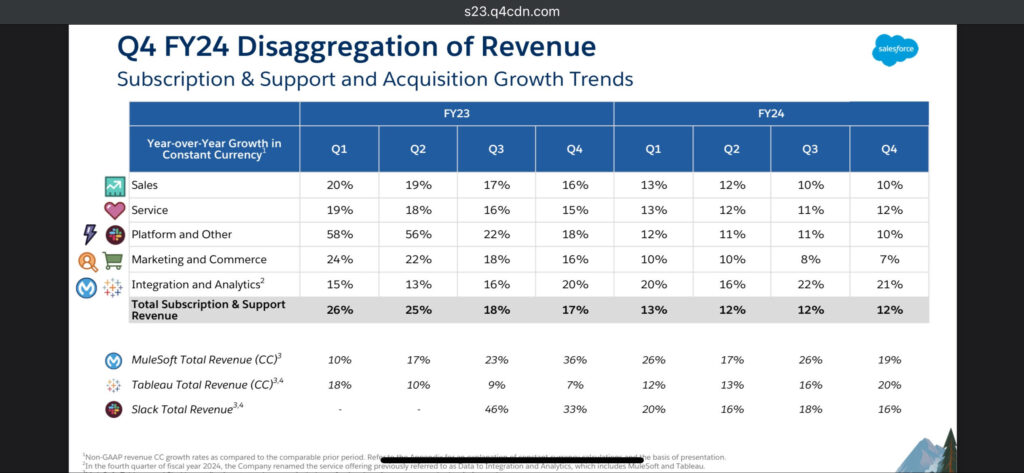

2) We then take a look at Salesforce’s earnings, where the Data Cloud is the Powerhouse of the earnings and CIOs are proving the value of data with their pocketbooks and the power of the purse. We break down the following earnings chart.

3) We saw NVIDIA’s success in AI as a sign that CIO budgets are changing. Find out about the new trend of CIO-led budgets that are independent of the traditional IT budget, as well as Charles’ framework of separating the efficiency bucket from the innovation bucket from his first book, The Quantum Age of IT.

4) One of the hottest companies in enterprise software sees a big leadership change, as Frank Slootman steps down from Snowflake and Sridhar Ramaswamy from the Neeva acquisition takes over. We discuss why this is a good move to avoid stagnation and discuss how to deal with bets in innovation.

5) Continuing the trend of innovation management, we talk about what Apple’s exit of the electric car business means in terms of managing innovative moonshots and what CIO’s often miss in terms of setting metrics around leadership and innovation culture.

6) And finally, we talk about the much-covered Google Gemini AI mistakes. We think the errors themselves fall within the range of issues that we’ve seen from other large language models, but we caution why the phrase “Eliminate Bias” should be a massive red flag for AI projects.

Today, we are kicking off a new podcast with our Chief Analyst Hyoun Park and The DX Report’s Charles Araujo. Together, we are looking at the biggest events in enterprise technology and discussing how they affect the CIO’s office. We’re planning to bring our decades of experience as market observers, hands-on technical skills, and strategic advisors not only to show what the big stories were, but also the big lessons that IT and other technical executives need to take from these stories.

If you want to learn how to avoid the biggest mistakes that CIOs will make across strategy, succession planning, innovation, budgeting, and integrating AI into existing technology environments, subscribe to our new video and podcast efforts! Check out Week 1 right here.

This week, we discuss in this episode the philosophy of fast-rising Zoho, an enterprise application company that has grown over 10x over the past decade to become a leading CRM and analytic software provider on a global basis based on our recent visit to Zoho’s Analyst Event in McAllen, Texas. Find out how “transnational localism” has supported Zoho’s global rocket-ship growth and what it means for managing your own international team.

We then TWIET about the Apple Vision Pro and how Apple, Meta, Microsoft, and Google have been pushing the boundaries of extended reality over the past decade as well as what this means for enterprise IT organizations based on Apple’s track record.

And finally we confront the complexities of Cloud FinOps and managing cloud costs at a time when layoffs are common in the tech world and IT economics and financial management are becoming increasingly complex.

The past week has been “Must See TV” in the tech world as AI darling OpenAI provided a season of Reality TV to rival anything created by Survivor, Big Brother, or the Kardashians. Although I often joke that my professional career has been defined by the well-known documentaries of “The West Wing,” “Pitch Perfect,” and “Sillcon Valley,” I’ve never been a big fan of the reality TV genre as the twist and turns felt too contrived and over the top… until now.

Starting on Friday, November 17th, when The Real Housewives of OpenAI started its massive internal feud, every organization working on an AI project has been watching to see what would become of the overnight sensation that turned AI into a household concept with the massively viral ChatGPT and related models and tools.

So, what the hell happened? And, more importantly, what does it mean for the organizations and enterprises seeking to enter the Era of AI and the combination of generative, conversational, language-driven, and graphic capabilities that are supported with the multi-billion parameter models that have opened up a wide variety of business processes to natural language driven interrogation, prioritization, and contextualization?

The Most Consequential Shake Up In Technology Since Steve Jobs Left Apple

The crux of the problem: OpenAI, the company we all know as the creator of ChatGPT and the technology provider for Microsoft’s Copilots, was fully controlled by another entity, OpenAI, the nonprofit. This nonprofit was driven by a mission of creating general artificial intelligence for all of humanity. The charter starts with“OpenAI’s mission is to ensure that artificial general intelligence (AGI) – by which we mean highly autonomous systems that outperform humans at most economically valuable work – benefits all of humanity. We will attempt to directly build safe and beneficial AGI, but will also consider our mission fulfilled if our work aids others to achieve this outcome.”

There is nothing in there about making money. Or building a multi-billion dollar company. Or providing resources to Big Tech. Or providing stakeholders with profit other than highly functional technology systems. In fact, further in the charter, it even states that if a competitor shows up with a project that is doing better at AGI, OpenAI commits to “stop competing with and start assisting this project.”

So, that was the primary focus of OpenAI. If anything, OpenAI was built to prevent large technology companies from being the primary force and owner of AI. In that context, four of the six board members of OpenAI decided that open AI‘s efforts to commercialize technology were in conflict with this mission, especially with the speed of going to market, and the shortcuts being made from a governance and research perspective.

As a result, they ended up firing both the CEO, Sam, Altman and removed President COO Greg Brockman, who had been responsible for architecting that resources and infrastructure associated with OpenAI, from the board. That action begat this rapid mess and chaos for this 700+ employee organization which was allegedly about to see an 80 billion dollar valuation

A Convoluted Timeline For The Real Housewives Of Silicon Valley

Friday: OpenAI’s board fires its CEO and kicks its president Greg Brockman off the board. CTO Mira Murati, who was called the night before, was appointed temporary CEO. Brockman steps down later that day.

Saturday: Employees are up in arms and several key employees leave the company, leading to immediate action by Microsoft going all the way up to CEO Satya Nadella to basically ask “what is going on? And what are you doing with our $10 billion commitment, you clowns?!” (Nadella probably did not use the word clowns, as he’s very respectful.)

Sunday: Altman comes in the office to negotiate with Microsoft and OpenAI’s investors. Meanwhile, OpenAI announces a new CEO, Emmett Shear, who was previously the CEO of video game streaming company Twitch. Immediately, everyone questions what he’ll actually be managing as employees threaten to quit, refuse to show up to an all-hands meeting, and show Altman overwhelming support on social media. A tumultuous Sunday ends with an announcement by Microsoft that Altman and Brockman will lead Microsoft’s AI group.

Monday: A letter shows up asking the current board to resign with over 700 employees threatening to quit and move to the Microsoft subsidiary run by Altman and Brockman. Co-signers include board member and OpenAI Ilya Sutskever, who was one of the four board votes to oust Altman in the first place.

Tuesday: The new CEO of OpenAI, Emmett Shear, states that he will quit if the OpenAI board can’t provide evidence of why they fired Sam Altman. Late that night, Sam Altman officially comes back to OpenAI as CEO with a new board consisting initially of Bret Taylor, former co-CEO of Salesforce, Larry Summers (former Secretary of the Treasury), and Adam d’Angelo, one of the former board members who voted to figure Sam Altman. Helen Toner of Georgetown and Tasha McCauley, both seen as ethical altruists who were firmly aligned with OpenAI’s original mission, both step down from the board.

Wednesday: Well, that’s today as I’m writing this out. Right now, there are still a lot of questions about the board, the current purpose of OpenAI, and the winners and losers.

Keep In Mind As We Consider This Wild And Crazy Ride

OpenAI was not designed to make money. Firing Altman may have been defensible from OpenAI’s charter perspective to build safe General AI for everyone and to avoid large tech oligopolies. But if that’s the case, OpenAI should not have taken Microsoft’s money. OpenAI wanted to have its cake and eat it as well with a board unused to managing donations and budgets at that scale.

Was firing Altman even the right move? One could argue that productization puts AI into more hands and helps prepare society for an AGI world. To manage and work with superintelligences, one must first integrate AI into one’s life and the work Altman was doing was putting AI into more people’s hands in preparation for the next stage of global access and interaction with superintelligence.

At the same time, the vast majority of current OpenAI employees are on the for-profit side and signed up, at least in part, because of the promise of a stock-based payout. I’m not saying that OpenAI employees don’t also care about ethical AI usage, but even the secondary market for OpenAI at a multi-billion dollar valuation would help pay for a lot of mortgages and college bills. But tanking the vast majority of employee financial expectations is always going to be a hard sell, especially if they have been sold on a profitable financial outcome.

OpenAI is expensive to run: probably well over 2 billion dollars per year, including the massive cloud bill. Any attempt to slow down AI development or reduce access to current AI tools needs to be tempered by the financial realities of covering costs. It is amazing to think that OpenAI’s board was so naïve that they could just get rid of the guy who was, in essence, their top fundraiser or revenue officer without worrying about how to cover that gap.

Primary research versus go-to-market activities are very different. Normally there is a church-and-state type of wall between these two areas exactly because they are to some extent at odds with each other. The work needed to make new, better, safer, and fundamentally different technology is often conflicted with the activity used to sell existing technology. And this is a division that has been well established for decades in academia where patented or protected technologies are monetized by a separate for-profit organization.

The Effective Altruism movement: this is an important catchphrase in the world of AI, as it is not just defined as a dictionary definition. This is a catchphrase for a specific view of developing artificial general intelligence (superintelligences beyond human capacity) with the goal of supporting a population of 10^58 millennia from now. This is one extreme of the AI world, which is countered by a “doomer” mindset thinking that AI will be the end of humanity.

Practically, most of us are in between with the understanding that we have been using superhuman forces in business since the Industrial Revolution. We have been using Google, Facebook, data warehouses, data lakes, and various statistical and machine learning models for a couple of decades that vastly exceed human data and analytic capabilities.

And the big drama question for me: What is Adam d’Angelo still doing on the board as someone who actively caused this disaster to happen? There is no way to get around the fact that this entire mess was due to a board-driven coup and he was part of the coup. It would be surprising to see him stick around for more than a few months especially now that Bret Taylor is on board, who provides an overlap of experiences and capabilities that d’Angelo possesses, but at greater scale.

The 13 Big Lessons We All Learned about AI, The Universe, and Everything

First, OpenAI needs better governance in several areas: board, technology, and productization.

Once OpenAI started building technologies with commercial repercussions, the delineation between the non-profit work and the technology commercialization needed to become much clearer. This line should have been crystal clear before OpenAI took a $10 billion commitment from Microsoft and should have been advised by a board of directors that had any semblance of experience in managing conflicts of interest at this level of revenue and valuation. In particular, Adam d’Angelo as the CEO of a multi-billion dollar valued company and Helen Toner of Georgetown should have helped to draw these lines and make them extremely clear for Sam Altman prior to this moment.

Investors and key stakeholders should never be completely surprised by a board announcement. The board should only take actions that have previously been communicated to all major stakeholders. Risks need to be defined beforehand when they are predictable. This conflict was predictable and, by all accounts, had been brewing for months. If you’re going to fire a CEO, make sure your stakeholders support you and that you can defend your stance.

You come at the king, you best not miss.” As Omar said in the famed show “The Wire,” you cannot try to take out the head of an organization unless your followup plan is tight.

OpenAI’s copyright challenges feel similar to when Napster first became popular as a streaming platform for music. We had to collectively figure out how to avoid digital piracy while maintaining the convenience that Napster provided for supporting music and sharing other files. Although the productivity benefits make generative AI worth experimenting with, always make sure that you have a back up process or capability for anything supported with generative AI.

OpenAI and other generative AI firms have also run into challenges regarding the potential copyright issues associated with their models. Although a number of companies are indemnifying clients from damages associated with any outputs associated with their models, companies will likely still have to stop using any models or outputs that end up being associated with copyrighted material.

From Amalgam Insights’ perspective, the challenge with some foundational models is that training data is used to build the parameters or modifiers associated with a model. This means that the copyrighted material is being used to help shape a product or service that is being offered on a commercial basis. Although there is no legal precedent either for or against this interpretation, the initial appearance of this language fits with the common sense definitions of enforcing copyright on a commercial basis. This is why the data collating approach that IBM has taken to generative AI is an important differentiator that may end up being meaningful.

Don’t take money if you’re not willing to accept the consequences. This is a common non-profit mistake to accept funding and simply hope it won’t affect the research. But the moment research is primarily dependent on one single funder, there will always be compromises. Make sure those compromises are expressly delineated in advance and if the research is worth doing under those circumstances.

Licensing nonprofit technologies and resources should not paralyze the core non-profit mission. Universities do this all the time! Somebody at OpenAI, both in the board and at the operational level, should be a genius at managing tech transfer and commercial utilization to help avoid conflicts between the two institutions. There is no reason that the OpenAI nonprofit should be hamstrung by the commercialization of its technology because there should be a structure in place to prevent or minimize conflicts of interest other than firing the CEO.

Second, there are also some important business lessons here.

Startups are inherently unstable. Although OpenAI is an extreme example, there are many other more prosaic examples of owners or boards who are unpredictable, uncontrollable, volatile, vindictive, or otherwise unmanageable in ways that force businesses to close up shop or to struggle operationally. This is part of the reason that half of new businesses fail within five years.

Loyalty matters, even in the world of tech. It is remarkable that Sam Altman was backed by over 90% of his team on a letter saying that they would follow him to Microsoft. This includes employees who were on visas and were not independently rich, but still believed in Sam Altman more than the organization that actually signed their paychecks. Although it never hurts to also have Microsoft’s Kevin Scott and Satya Nadella in your corner and to be able to match compensation packages, this also speaks to the executive responsibility to build trust by creating a better scenario for your employees than others can provide. In this Game of Thrones, Sam Altman took down every contender to the throne in a matter of hours.

Microsoft has most likely pulled off a transaction that ends up being all but an acquisition of OpenAI. It looks like Microsoft will end up with the vast majority of OpenAI’s‘s talent as well as an unlimited license to all technology developed by OpenAI. Considering that OpenAI was about to support a stock offering with an $80 billion market cap, that’s quite the bargain for Microsoft. In particular, Bret Taylor’s ascension to the board is telling as his work at Twitter was in the best interests of the shareholders of Twitter in accepting and forcing an acquisition that was well in excess of the publicly-held value of the company. Similarly, Larry Summers, as the former president of Harvard University, is experienced in balancing non-profit concerns with the extremely lucrative business of Harvard’s endowment and intellectual property. As this board is expanded to as many as nine members, expect more of a focus on OpenAI as a for-profit entity.

With Microsoft bringing OpenAI closer to the fold, other big tech companies that have made recent investments in generative AI now have to bring those partners closer to the core business. Salesforce, NVIDIA, Alphabet, Amazon, Databricks, SAP, and ServiceNow have all made big investments in generative AI and need to lock down their access to generative AI models, processors, and relevant data. Everyone is betting on their AI strategy to be a growth engine over the next five years and none can afford a significant misstep.

Satya Nadella’s handling of the situation shows why he is one of the greatest CEOs in business history. This weekend could have easily been an immense failure and a stock price toppling event for Microsoft. But in a clutch situation, Satya Nadella personally came in with his executive team to negotiate a landing for openAI, and to provide a scenario that would be palatable both to the market and for clients. The greatest CEOs have both the strategic skills to prepare for the future and the tactical skills to deal with immediate crisis. Nadella passes with flying colors on all accounts and proves once again that behind the velvet glove of Nadella’s humility and political savvy is an iron fist of geopolitical and financial power that is deftly wielded.

Carefully analyze AI firms that may have similar charters for supporting safe AI, and potentially slowing down or stopping product development for the sake of a higher purpose. OpenAI ran into challenges in trying to interpret its charter, but the charter’s language is pretty straightforward for anyone who did their due diligence and took the language seriously. Assume that people mean what they say. Also, consider that there are other AI firms that have similar philosophies to OpenAI, such as Anthropic, which spun off of OpenAI for reasons similar to the OpenAI board reasoning of firing Sam Altman. Although it is unlikely that Anthropic (or large firms with safety-first philosophies like Alphabet and Meta’s AI teams) will fall apart similarly, the charters and missions of each organization should be taken into account in considering their potential productization of AI technologies.

AI is still an emerging technology. Diversify, diversify, diversify. It is important to diversify your portfolio and make sure that you were able to duplicate experiments on multiple foundation models when possible. The marginal cost of supporting duplicate projects pales in comparison to the need to support continuity and gain greater understanding of the breath of AI output possibilities. With the variety of large language models, software vendor products, and machine learning platforms on the market, this is a good time to experiment with multiple vendors while designing process automation and language analysis use cases.

Over the past year, Generative AI has taken the world by storm as a variety of large language models (LLMs) appeared to solve a wide variety of challenges based on basic language prompts and questions.

A partial list of market-leading LLMs currently available include:

The biggest question regarding all of these models is simple: how to get the most value out of them. And most users fail because they are unused to the most basic concept of a large language model: they are designed to be linguistic copycats.

As Andrej Karpathy of OpenAI stated earlier this year,

And we all laughed at the concept for being clever as we started using tools like ChatGPT, but most of us did not take this seriously. If English really is being used as a programming language, what does this mean for the prompts that we use to request content and formatting?

I think we haven’t fully thought out what it means for English to be a programming language either in terms of how to “prompt” or ask the model how to do things correctly or how to think about the assumptions that an LLM has as a massive block of text that is otherwise disconnected from the real world and lacks the sensory input or broad-based access to new data that can allow it to “know” current language trends.

Here are 8 core language-based concepts to keep in mind when using LLMs or considering the use of LLMs to support business processes, automation, and relevant insights.

1) Language and linguistics tools are the relationships that define the quality of output: grammar, semantics, semiotics, taxonomies, and rhetorical flourishes. There is a big difference between asking for “write 200 words on Shakespeare” vs. “elucidate 200 words on the value of Shakespeare as a playwright, as a poet, and as a philosopher based on the perspective on Edmund Malone and the English traditions associated with blank verse and iambic pentameter as a preamble to introducing the Shakespeare Theatre Association.”

I have been a critic of the quality that LLMs provide from an output perspective, most recently in my perspective “Instant Mediocrity: A Business Guide to ChatGPT in the Enterprise.” https://amalgaminsights.com/2023/06/06/instant-mediocrity-a-business-guide-to-chatgpt-in-the-enterprise/. But I readily acknowledge that the outputs one can get from LLMs will improve. Expert context will provide better results than prompts that lack subject matter knowledge

2) Linguistic copycats are limited by the rules of language that are defined within their model. Asking linguistic copycats to provide language formats or usage that are not commonly used online or in formal writing will be a challenge. Poetic structures or textual formats referenced must reside within the knowledge of the texts that the model has seen. However, since Wikipedia is a source for most of these LLMs, a contextual foundation exists to reference many frequently used frameworks.

3) Linguistic copycats are limited by the frequency of vocabulary usage that they are trained on. It is challenging to get an LLM to use expert-level vocabulary or jargon to answer prompts because the LLM will typically settle for the most commonly used language associated with a topic rather than elevated or specific terms.

This propensity to choose the most common language associated with a topic makes it difficult for LLM-based content to sound unique or have specific rhetorical flourishes without significant work from the prompt writer.

4) Take a deep breath and work on this. Linguistic copycats respond to the scope, tone, and role mentioned in a prompt. A recent study found that, across a variety of LLM’s, the prompt that provided the best answer for solving a math problem and providing instructions was not a straightforward request such as “Let’s think step by step,” but “Take a deep breath and work on this problem step-by-step.”

Using a language-based perspective, this makes sense. The explanations of mathematical problems that include some language about relaxing or not stressing would likely be designed to be more thorough and make sure the reader was not being left behind at any step. The language used in a prompt should represent the type of response that the user is seeking.

5) Linguistic copycats only respond to the prompt and the associated prompt engineering, custom instructions, and retrieval data that they can access. It is easy to get carried away with the rapid creation of text that LLM’s provide and mistake this for something resembling consciousness, but the response being created is a combination of grammatical logic and the computational ability to take billions of parameters into account across possibly a million or more different documents. This ability to access relationships across 500 or more gigabytes of information is where LLMs do truly have an advantage over human beings.

6) Linguistic robots can only respond based on their underlying attention mechanisms that define their autocompletion and content creation responses. In other words, linguistic robots make judgment calls on which words are more important to focus on in a sentence or question and use that as the base of the reply.

For instance, in the sentence “The cat, who happens to be blue, sits in my shoe,” linguistic robots will focus on the subject “cat” as the most important part of this sentence. The cat “happens to be,” implies that this isn’t the most important trait. The cat is blue. The cat sits. The cat is in my shoe. The words include an internal rhyme and are fairly nonsensical. And then the next stage of this process is to autocomplete a response based on the context provided in the prompt.

7) Linguistic robots are limited by a token limit for inputs and outputs. Typically, a token is about four characters while the average English content word is about 6.5 characters (https://core.ac.uk/download/pdf/82753461.pdf). So, when an LLM talks about supporting 2048 tokens, that can be seen as about 1260 words, or about four pages of text, for concepts that require a lot of content. In general, think of a page of content as being about 500 tokens and a minute of discussion typically being around 200 tokens when one is trying to judge how much content is either being created or entered into an LLM.

8) Every language is dynamic and evolves over time. LLMs that provide good results today may provide significantly better or worse results tomorrow simply because language usage has changed or because there are significant changes in the sentiment of a word. For instance, the English language word “trump” in 2015 has a variety of political relationships and emotional associations that are now standard to language usage in 2023. Be aware of these changes across languages and time periods in making requests, as seemingly innocuous and commonly used words can quickly gain new meanings that may not be obvious, especially to non-native speakers.

Conclusion

The most important takeaway of the now-famous Karpathy quote is to take it seriously not only in terms of using English as a programming language to access structures and conceptual frameworks, but also to understand that there are many varied nuances built into the usage of the English language. LLM’s often incorporate these nuances even if those nuances haven’t been directly built into models, simply based on the repetition of linguistic, rhetorical, and symbolic language usage associated with specific topics.

From a practical perspective, this means that the more context and expertise provided in asking an LLM for information and expected outputs, the better the answer that will typically be provided. As one writes prompts for LLMs and seek the best possible response, Amalgam Insights recommends providing the following details in any prompt:

Tone, role, and format: This should include a sentence that shows, by example, the type of tone you want. It should explain who you are or who you are writing for. And it should provide a form or structure for the output (essay, poem, set of instructions, etc…). For example, “OK, let’s go slow and figure this out. I’m a data analyst with a lot of experience in SQL, but very little understanding of Python. Walk me through this so that I can explain this to a third grader.”

Topic, output, and length: Most prompts start with the topic or only include the topic. But it is important to also include perspective on the size of the output. Example, “I would like a step by step description of how to extract specific sections from a text file into a separate file. Each instruction should be relatively short and comprehensible to someone without formal coding experience.”

Frameworks and concepts to incorporate: This can include any commonly known process or structure that is documented, such as an Eisenhower Diagram, Porter’s Five Forces, or the Overton Window. As a simpe example, one could ask, “In describing each step, compare each step to the creation of a pizza, wherever possible.”

Combining these three sections together into a prompt should provide a response that is encouraging, relatively easy to understand, and compares the code to creating a pizza.

In adapting business processes based on LLMs to make information more readily available for employees and other stakeholders, be aware of these biases, foibles, and characteristics associated with prompts as your company explores this novel user interface and user experience.

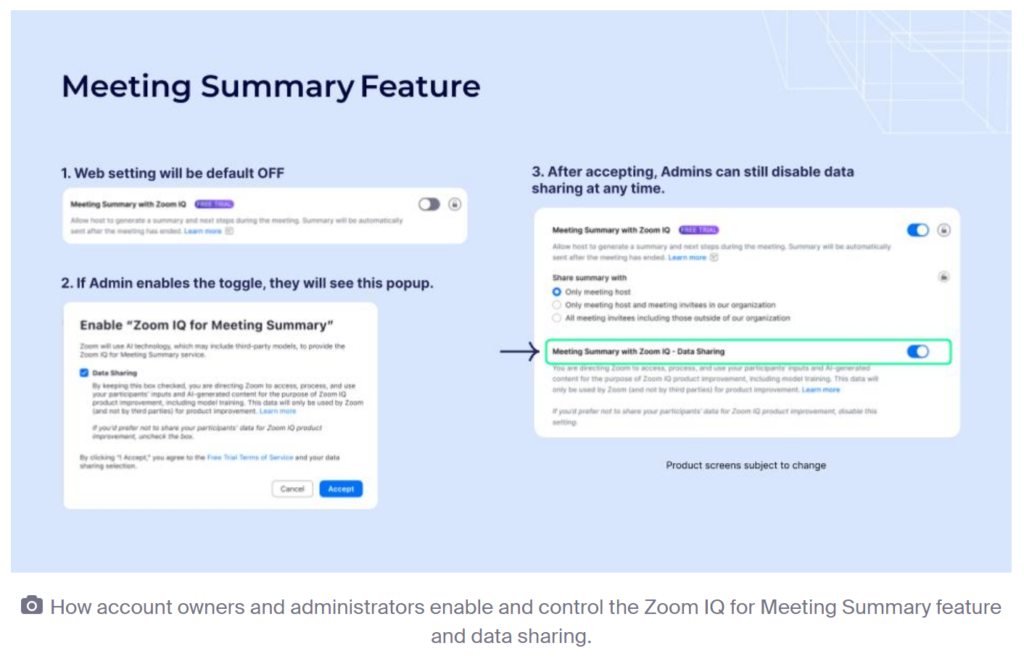

Note: This piece was accurate as of the time it was written, but on August 11th, Zoom edited its Service Agreement to remove the most egregious claims around content ownership. Its current language is more focused on the limited license needed to deliver content and establishes that user content is owned by the user. Amalgam Insights considers the changes made as of August 11th to be more in-line both with industry standards and with enterprise compliance concerns.

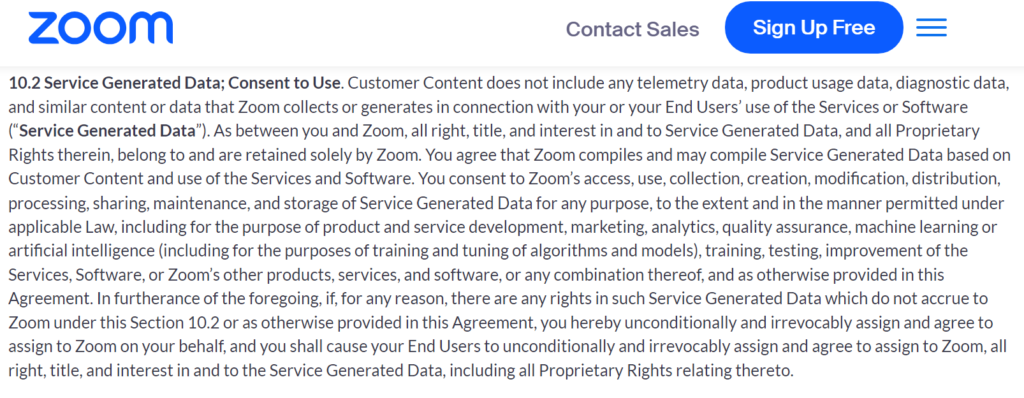

On August 7, 2023, Zoom announced a change to its terms and conditions in response to language discovered in Zoom’s service agreement that gave Zoom nearly unlimited capability to collect data and an unlimited license to use this information going forward for any commercial use. In doing so, Zoom has brought up a variety of intellectual property and AI issues that are important for every software vendor, IT department, and software sourcing group to consider over the next 12-18 months.

Analyzing Zoom’s Service Agreement Language

This discovery seems to have been a few months in the making as these changes seem to have initially been made back in March 2023 as it was launching some AI capabilities. Looking at each section, we can see that 10.2 and 10.3 focus on the usage of data.

Although this data usage may seem aggressive at first, one has to understand that Zoom‘s primary function is video conferencing, which requires moving both video and audio data across multiple servers to get from one point to another. This requires Zoom to have broad permission to transfer all data involved in a standard video, conference, or webinar, which includes all the data being used and all of the service data created. So, in this case, Amalgam Insights believes this access to data is not such a big deal as Zoom probably needed to update this language simply to support even basic augments, such as cleaning up audio or improving visual quality with any sort of artificial or machine learning capabilities.

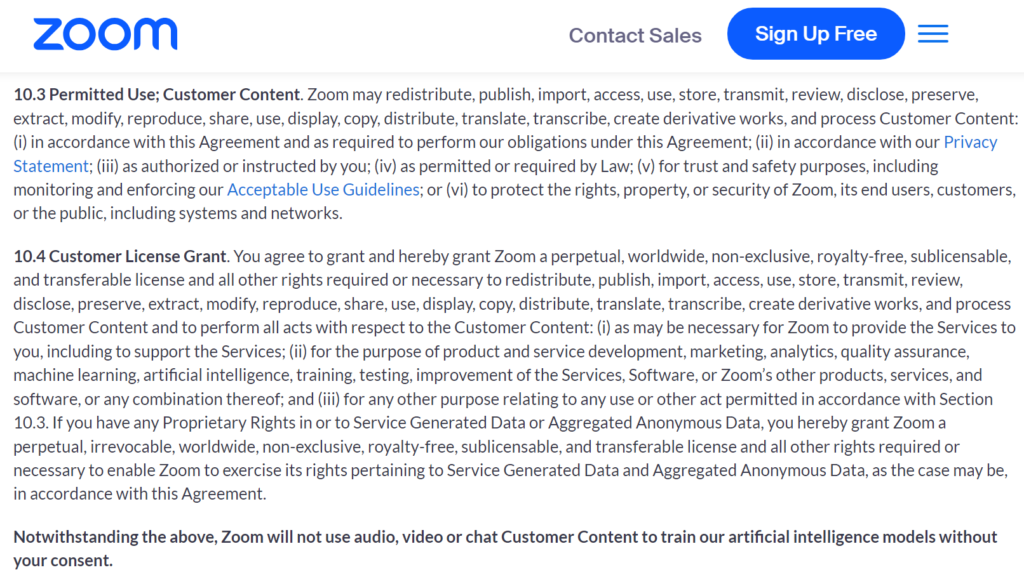

However, in Amalgam, insights perspective, 10.4 is of much more aggressive set of terms. This change provides Zoom with a broad-ranging commercial license to any data used on Zoom‘s platform. This means that your face, your voice, and any trade, secrets, patents, or trademarks used on Zoom now become commercially usable by Zoom. Whether this was the intention or not, this section both sounds aggressive and crosses the line on the treatment that companies expect for their own data.

This is an extremely aggressive stance by most intellectual property standards. And it stands out as conflicting in comparison, to how data is positioned by Microsoft and Salesforce, enterprise application platform companies that aren’t exactly considered innocent or naïve in terms of running a business.

What went wrong here? Zoom is traditionally known as a company that is for the most part end user-centric. Zoom’s mission includes the goal, to “improve the quality and effectiveness of communications. We deliver happiness.” And Eric Yuan’s early stories about wanting to speak with loved ones remotely and refusing to do on-site meetings in promoting the power of remote meetings are part of the Zoom legend.

However, Zoom is also facing the challenge of meeting institutional shareholder demands to increase stock value. When Zoom’s stock rose in the pandemic, it reached such amazing heights that it led to extreme pressure for Zoom to figure out how to 5X or 10X their company revenue quickly. Knowing that the stock was in a bit of a bubble, Zoom initially tried to purchase Five9, a top-notch cloud contact center solution, but ran into problems during the acquisition process as the stock prices of each company ended up being too volatile to come to an agreement on both the value and price of the stock involved.

And I speculate that at this point Zoom is focused on bringing its stock back up to pandemic heights, a bubble that may honestly never be reached again. For Zoom, 2020 was a dot-com-like event, where its valuation wildly exceeded its revenue. And as other video conferencing, and event software solutions ended up quickly improving their products, Zoom’s core conferencing capabilities started to be seen as a somewhat commoditized capability.

Following the mission of the company would have meant looking more deeply at communications-based processes, collaboration, transcription, and perhaps even emoji and social media enhancement: all of the ways that we communicate with each other. But, the problem is that there is really only one play right now that can quickly leads to a doubling or tripling of stock price and that is AI. There’s no doubt that the amount of video and audio that Zoom processes on a daily basis can train a massive language model, as well as other machine learning models focused on re-creating and enhancing video and audio.

Positioned in a way where it was understood that Zoom would enhance current communicative capabilities, it could’ve been a very positive announcement for Zoom to talk about new AI capabilities. Zoom has taken initial steps to integrate AI into Zoom with Meeting Summary and Team Chat Compose products. But given the limited capabilities of these products, the licensing language used in the service agreement seems excessive.

The language used in section 10 of Zoom’s service agreement is very clear about maintaining the right to license and commercialized all aspects of any data collected by Zoom. And that statement has not been modified. Whether this is because of an overactive lawyer or Zoom’s future ambitions, or promises made to a board or institutional investors is beyond my pay grade and visibility. But I do know that that phrase is obviously not user-friendly, and Zoom is not providing visibility to those changes at the administrative level. The language and buttons used to support zooms, a model and commercialization efforts are very different on the administrative page compared to the language used in the service agreement.

Image from Zoom’s August 7th blog post

Understanding that legal language can take time to change, it makes sense to wait a few days to see if Zoom reverts to prior language or further modifies section 10 to represent a more user-friendly and client-friendly promise. And I think this language reflects a couple of issues that go far beyond Zoom.

First, service agreements for software companies in general, are often treated as an exercise in providing companies with maximum flexibility, while taking away basic rights from end users. This is not just a product management issue; this is an industry issue where this language and behavior is considered status quo both in the technology industry and in the legal profession. When companies like Alphabet and Meta, previously Facebook, were able to get away with the level of data collection associated with supporting each free user without facing governance or compliance consequences in most of the world, that set a standard for tech companies’ corporate counsel. Honestly, the language used in Zoom‘s current service agreement as of August 7, 2023 is not out of scope for many companies in the consumer world that provide social technologies.

The second issue is the overwhelming pressure that exists to be first or early to market in AI. The remarkable success of ChatGPT and other open AI-related models has shown that there is demand for AI that is either interesting or useful and can be easily used and accessed by the typical user or customer. This demand is especially high for any company that has a significant amount of text, data, audio, or video. The recent March 2023 announcement of Bloomberg GPT is only the starting point of what will be a wide variety of custom language, models and machine learning models that come to market over the next 12 to 18 months. Zoom obviously wants to be part of that discussion, and there are other companies, such as Microsoft, Adobe and Alphabet as well as noted start-ups like OpenAI that have done amazing AI work with audio and video already. Part of the reason that this stands out is that Zoom is one of the first companies to change its policies and aggressively seek a permanent commercial license associated with all user content and forcing and opt-out process that lacks auditability or documentation regarding how users can trust that their data is no longer being used to train models or support any other commercial activities Zoom may wish to pursue. But Amalgam Insights is absolutely sure that Zoom will not be the last company to do this by any means. This language and the response should also serve as both a warning and a lesson to all other companies, seeking to significantly change their service agreements to support AI projects.

What is next for Zoom?

From Amalgam Insights’ perspective, there are three potential directions that Zoom can pursue going forward.

One, do nothing or make minimal changes to the current policy. Consumer and social media-based technology policies have set a precedent for the level of data and licensing access in Zoom’s service agreement, but this level of customer data usage is considered extreme in most business software agreements. Will Zoom end up being a test case for pushing the boundaries for business data use? This seems unlikely given that Zoom has not traditionally been considered an aggressive company in pushing customer norms. Zoom does try to move fast and scale fast, but Zoom’s mistakes have typically been more due to incomplete processes rather than acts of commission and intentionally trying to push boundaries.

Two, rewrite parts of Section 10 that are intrusive from a licensing and commercial usage perspective. Amalgam Insights hopes that this is an opportunity for Zoom to lead from an end user licensing or service agreement perspective in making agreements more transparent and in using more exact legal language that feels cooperative instead of coercive. The legal approach of including all possible scenarios may be considered professionally competent, but the business optics are antagonistic.

Three, come out with an explicit enterprise version of technology that is not managed under these current rules set in section 10 so that data is not explicitly used for models and cannot easily be turned on through a simple toggle switch in the administration console. As my friend and data management analyst extraordinaire Tony Baer stated on LinkedIn (where you should be following him) “The solution for Zoom is to be more explicit: an enterprise version where data, no matter how anonymized, is not shared for Generative AI or any other Zoom commercial purpose whatsoever, and maybe a more general and/or freemium edition (which is how many consumers have already been roped in) where Zoom can do its Gen AI thing.”

Recommendations

The first recommendation is actually aimed towards the CIO office, procurement office, and other software purchasers. Be aware that your software provider is going to pursue AI and will likely need to change terms and conditions associated with your account to do so. This is a challenge, as multinational enterprises now face the possibility of approaching or exceeding 1,000 apps and data sources under management and even businesses of 250 employees or less average one app per employee. There is a massive race towards aggregating data, building custom AI models, and commercializing the outputs as benchmarks, workflows, automation, and guidance. But Zoom is not a one-off situation and your organization isn’t going to escape the issues brought up in Zoom’s service agreement language just by moving to another provider. This is an endemic and market-wide challenge, far beyond what Zoom is experiencing.

The second recommendation: One solution to this problem may be for vendors to split their product into public consumer-facing products and private products from a EULA and terms and conditions perspective. This wouldn’t be the worst approach, and would maintain the consumer expectation of free services that are subsidized by data and access while giving businesses, the confidence that they are working with a solution that will protect their intellectual property from being accessed or recreated by a machine learning model. This also potentially allows for more transparency in legal language as this product split is considered. Tech lawyer Cathy Gellis, stated “There can be the lawyerly temptation to phrase them (terms of service) as broadly as possible to give you the most flexibility as you continue to develop your service. But the problem with trying to proactively obtain as many permissions as you can is that users may start to think you will actually use them and react to that possibility.” In 2023, software vendors should assume that corporate clients will be wary of any language that puts trade secrets, patents, trademarks, or personally identifiable information at risk. Any changes to terms of service or service agreements should be reviewed both from a buy-side and sell-side perspective. This may include bringing in procurement or specialized software purchasing teams to reflect the customer’s perspective.

The third recommendation goes back to the ethical AI work that Amalgam Insights did several years ago. AI must be conducted in context of the same culture and goals that are considered pervasive within the company. Any AI policy that goes significantly outside the culture, norms, and expectations of the company will stand out. And this can be a challenge, because AI has been treated as an experiment in many cases, rather than as a formalized, technical capability. As AI development and policy is shaped, this is a time when new products, governance, and documentation need to be tightly aligned to core business and mission principles. AI is a test of every company’s culture and purpose and this is a time when the corporate ability to execute on lofty qualitative ideals will be actively challenged.

Zoom’s misstep in aggressively pursuing rights and access to client data should not just be seen as a specific organizational misstep, but as part of a set of trends that are important for enterprise, IT, purchasing, and legal departments as well as all software and data source vendors seeking to pursue AI and further monetize deep digital assets. The next 12 to 18 months are going to be a wild time in the technology market as every software vendor pursues some sort of AI strategy, and there will be mountains of new legal language, technical capabilities, and compliance aspects to review.